Navigating today’s intricate healthcare landscape poses significant challenges for consumers seeking prescription medications. Despite legislative efforts, notably the Consolidated Appropriations Act 2021 which aimed for improvements, policymakers clearly missed the mark as dissatisfaction remains widespread.

Rising drug prices, opaque practices by Pharmacy Benefit Managers (PBM) and barriers to access continue to permeate a complex and daunting environment at the expense of the consumer.

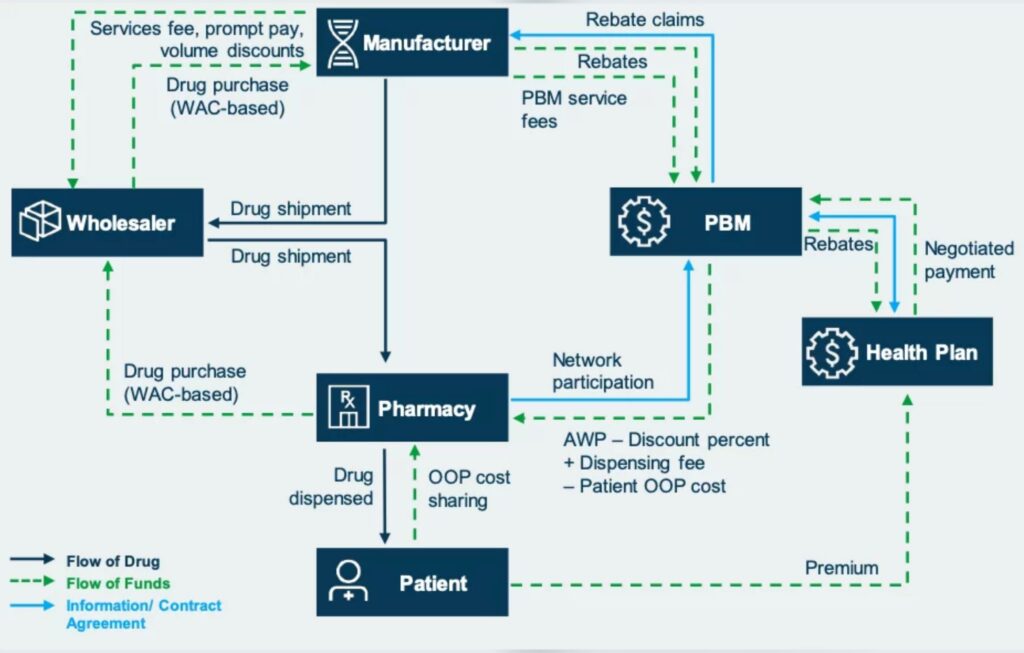

Transparency and consumer advocacy are necessary elements that will promote positive change within this murky pharmaceutical maze. At the heart of this labyrinth lies the Pharmacy Benefit Managers (PBM), a cornerstone component of the supply chain.

Flow chart by Avalere

Six PBMs control 96% of the prescription drug market. They are vertically integrated healthcare empires. Global market share is projected to grow from $540.32 billion in 2023 to $809.79 billion by 2030. Three of the largest are: CVS, who reported $357.8 billion of revenue in 2023, Cigna/Express Scripts, who reported $195 billion and Optum Rx, whose revenues were $116.10 billion.

PBMs oversee various aspects of prescription drug benefits on behalf of health insurance plans and employers. They act as intermediaries between manufacturers, health insurers, pharmacies and patients. This includes bundled services such as developing formularies, processing claims, administering pharmacy networks, implementing utilization management (i.e. step therapies; prior authorizations) and providing clinical support services.

Where it Begins

Drug manufacturers undoubtedly play a crucial role in saving lives. The reality is, drug companies are also running a business. $6.88 billion US dollars were spent in pharmaceutical advertisements in 2021. The Congressional Budget Office reported that the industry dedicated $83 billion to Research and Development in 2019. Colossal amounts of money are exchanged annually within this industry as it continues to grow at a breakneck speed.

Enters the PBMs’ covert sister companies [these are offshore by the way], known as rebate aggregators. Manufacturers are pressured into providing rebates to ensure their products are placed favorably within the PBMs’ drug formulary. Implementing prior authorization requirements; setting the drug’s copay levels (tiers), PBMs prioritize formulary placement based on potential rebates, rather than the drug’s effectiveness.

More opacity transpires when Direct and Indirect Remuneration (DIR) fees are imposed on pharmacies within PBM networks. These fees are intended to recoup additional costs based on factors such as performance metrics, network management and rebate arrangements, yet DIR fees unfortunately leave the sickest citizens bearing the brunt of artificially inflated coinsurance and copayments.

Other known practices such as spread pricing, fuels profit and furthers confusion. Spread pricing entails charging health plans or insurance companies more for prescription drugs than what PBMs reimburse pharmacies. The difference between what PBMs pay pharmacies and what they charge health plans is known as the “spread.”

Further barriers and ambiguity occur as PBMs are allowed to restrict networks, which mandate patients to utilize specific pharmacies to obtain their specialty medications. Such a practice limits patient options and could lead to extended waiting periods for medication delivery, especially for those residing in rural or underserved regions. Factoid: specialty drugs represent 50% of overall drug spend.

The concentrated power within this mammoth supply chain has become dangerously too vast to manage. It is imperative that citizens gain a greater understanding of what is happening through transparency and advocacy.

Where is the Remedy?

Advocating for reform in prescription drug practices emerges as the crucial first step. Change begins by amplifying voices and demanding accountability from industry stakeholders. Consumers can empower themselves by learning more about prescription drug pricing and lobbying policymakers for meaningful reforms while supporting organizations that champion healthcare affordability.

Consumers can get involved and learn more:

Families USA: (familiesusa.org) a nonprofit focusing on healthcare advocacy, with a mission to ensure affordability and access to high-quality healthcare, including prescription drugs, for all Americans.

National Consumers League: (nclnet.org) a nonprofit advocacy organization that focuses on consumer rights and protections. NCL advocates for policies that promote transparency, affordability, and safety in the prescription drug market.

Key Industry Terms

AWP: Average Wholesale Price is a benchmark used in the pharmaceutical industry to determine the reimbursement rates for prescription drugs.

DIR: Direct and Indirect Remuneration refers to a type of fee imposed by Pharmacy Benefit Managers on pharmacies participating in their networks.

Formulary: a list of generic and brand name drugs covered by a health plan.

List price: Also referred to as the wholesale acquisition cost (WAC), denotes the manufacturer’s price for a drug or biologic, excluding any discounts extended to wholesalers, PBMs or other buyers.

OOP: Out of Pocket

Rebate: A concession provided by a drug manufacturer to an insurer or PBM; these discounts may be partially or fully passed on from PBMs to insurers.

Spread pricing involves a payment structure where a PBM reimburses a network pharmacy an amount less than what the insurer pays to the PBM for a drug, with the PBM keeping the difference as profit.

Tier: A category of drugs within a formulary subject to a specific cost-sharing arrangement for plan enrollees; formularies typically have several tiers with different cost-sharing structures for each tier. Lower tiers require lower cost sharing.